Published: 16 March 2026. The English Chronicle Desk. The English Chronicle Online.

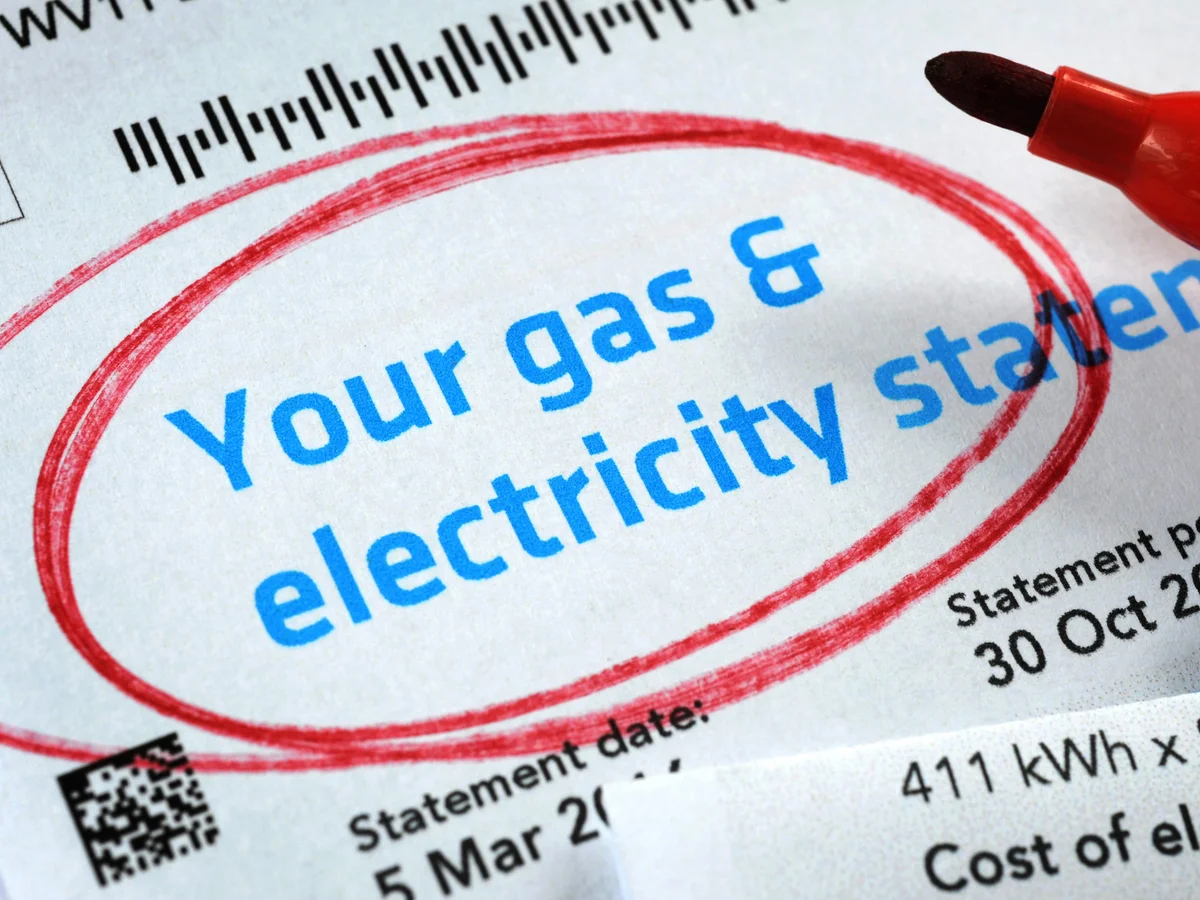

The landscape of British household finance is undergoing a profound and troubling shift as essential UK bills become an insurmountable mountain for millions of people across the country. According to the latest comprehensive data released by the debt charity StepChange, the struggle to keep up with basic living costs has now transitioned from a temporary crisis into a permanent state of existence. This phenomenon is being described by leading campaigners as the new normal for a significant portion of the population. Families who once managed to balance their books are now finding themselves trapped in a cycle of persistent arrears that shows no signs of abating. The figures provided by the charity highlight a worrying trend where the cost of simply existing is outstripping the average income of low-income households. This systemic issue is not merely a reflection of poor financial management but rather a symptom of a deeply fractured economic environment.

As we move through 2026, the data confirms that average arrears for housing, utilities, and council tax all surged over the past twelve months. Despite a general stabilization in the wider economy, the legacy of several years of high inflation continues to weigh heavily on the most vulnerable. People have faced a relentless barrage of price increases for essential goods and services which has left their budgets stretched to a breaking point. Furthermore, the ongoing geopolitical instability in the Middle East has cast a long shadow over energy markets, sparking renewed fears of fresh price hikes in the near future. This constant state of uncertainty makes it nearly impossible for families to plan for their financial recovery. StepChange reports that their clients are already grappling with significant debt burdens that have grown even as the pace of price increases began to slow down.

The housing sector remains one of the most significant contributors to the current debt crisis affecting many UK residents today. While the rapid growth in mortgage costs and rental prices appeared to decelerate throughout 2025, the actual amount of debt owed by individuals continued to climb. Average rent arrears rose by an alarming fifteen percent over the last year, reaching a total of two thousand three hundred and seventy-two pounds. Even more concerning is the situation for those with mortgages, where average arrears jumped by twenty-two percent in a single year. These figures represent more than just numbers on a balance sheet; they signify a genuine risk of homelessness for thousands of families. When housing costs become unaffordable, the stability of the entire household is compromised, leading to a cascade of other financial and social problems.

Energy costs continue to represent a massive hurdle for households trying to manage their essential UK bills effectively this year. Although prices have retreated from the record peaks seen back in 2022, the debt associated with heating and lighting remains incredibly high. StepChange indicates that over a third of their clients are currently in debt to their energy suppliers, a figure that remains stubbornly high. While the percentage of people in arrears fell slightly compared to 2024, the average amount of debt actually grew by over two hundred pounds. This suggests that while fewer people are falling behind, those who are in debt are falling much deeper into the red. The average energy debt now stands at two thousand five hundred and sixty pounds per household. Such a significant sum is often impossible to clear without substantial changes to income or direct government intervention.

The demographic profile of those seeking help provides a clear picture of who is being hit hardest by these economic pressures. Two in five clients seen by the debt charity over the last year were recipients of universal credit, highlighting the inadequacy of current benefit levels. Additionally, three in five people seeking assistance were living in rented accommodation, where they have little control over their living environment. Vikki Brownridge, the chief executive at StepChange, has been vocal about the devastating impact of these trends on the British public. She emphasizes that the rising cost of everyday essentials remains prohibitively high for many households regardless of their efforts to save. Her observations reflect a reality where even the most disciplined spenders cannot keep up with the soaring prices of basic necessities. The pressure has been building for several years, and the latest data shows that household arrears are showing little sign of slowing down.

To combat this escalating crisis, campaigners are calling for immediate and decisive action from the government to protect the most vulnerable. The charity is advocating for the introduction of national social tariffs for both energy and water to ensure affordability. These tariffs would be specifically designed to bring costs back down to a level that is manageable for those on low incomes. Without such targeted support, many people will continue to fall into debt just to meet their basic requirements for survival. The argument is that essential services should not be a luxury that only the wealthy can afford without stress. By implementing social tariffs, the government could provide a much-needed safety net that prevents families from falling into a spiral of permanent debt. This approach would recognize that the current market mechanisms are failing to provide for the fundamental needs of the population.

The psychological toll of living with persistent debt is another critical factor that cannot be ignored in this discussion. Financial stress is a leading cause of mental health issues, which in turn can impact a person’s ability to work and earn. This creates a vicious cycle where debt leads to illness, and illness leads to further financial decline. Many people reporting high essential UK bills also describe feelings of hopelessness and isolation as they struggle to keep their heads above water. The social fabric of communities is also under threat as more people withdraw from participation due to a lack of disposable income. Ensuring that basic bills are affordable is therefore not just an economic necessity but a vital public health requirement. A society where the majority of citizens are constantly worried about their next utility bill is not a sustainable or healthy one.

Looking ahead, the role of consumer credit debt is also becoming more prominent as people use loans to bridge the gap. When income does not cover essential UK bills, many individuals turn to credit cards or high-interest loans to pay for food and heat. This temporary fix only serves to increase the total debt burden in the long run, making the eventual recovery even harder. StepChange has noted that the integration of housing, energy, and consumer credit debt is now a standard feature of their clients’ finances. This complexity makes the task of debt advice more challenging and the path to financial freedom much longer. There is a growing consensus that a holistic approach is needed to tackle the root causes of this widespread financial instability. Providing advice alone is no longer enough when the underlying math of household income simply does not add up.

As we analyze the current situation, it is clear that the traditional methods of managing debt are being tested like never before. The sheer scale of the arrears across all sectors suggests that this is a structural issue within the UK economy. Fairness and responsibility must be at the heart of any proposed solutions to ensure that no one is left behind. The government, utility companies, and financial institutions all have a role to play in creating a more resilient financial system. Whether through the implementation of social tariffs or the reform of the benefit system, the goal must be to end the new normal of debt. Addressing these challenges requires a level of political will and social empathy that matches the gravity of the situation facing millions of households today.

In conclusion, the report from StepChange serves as a stark reminder of the financial pressures that define modern life for many in Britain. The rise in arrears for housing and utilities is a clear indication that the cost-of-living crisis has evolved into a long-term economic challenge. While the numbers are daunting, they also provide a roadmap for the interventions that are most urgently required by the public. By focusing on the affordability of essential UK bills, there is a chance to reverse these trends and provide a more stable future. It is a call to action for everyone involved in the economy to prioritize the well-being of the most vulnerable citizens. Only through collective effort and systemic change can we hope to move past this period of financial hardship and restore a sense of security to British homes.

Related News:

Green Party Surges Past Labour in Latest UK Poll

Green Party Surges Past Labour in Latest UK Poll

Army Officers Orders to Cut Ties with Men-Only Clubs

Army Officers Orders to Cut Ties with Men-Only Clubs

Trump’s UK Ambassador Urges North Sea Drilling to Strengthen US Ties

Trump’s UK Ambassador Urges North Sea Drilling to Strengthen US Ties

French Taxi Driver Cleared in David Lammy Theft Case After Fare Dispute

French Taxi Driver Cleared in David Lammy Theft Case After Fare Dispute

Labour immigration crackdown could cost UK £4.4bn

BBC to Apologise Over Edited Trump Speech Amid Backlash

Labour immigration crackdown could cost UK £4.4bn

BBC to Apologise Over Edited Trump Speech Amid Backlash

Britain deploys RAF specialists to assist Belgium with drone threats

Britain deploys RAF specialists to assist Belgium with drone threats

Millionaires group urge Reeves to introduce wealth tax to ‘lift kids out of poverty’

Millionaires group urge Reeves to introduce wealth tax to ‘lift kids out of poverty’

Starmer Faces Growing Dissent as Labour MPs Weigh Leadership Challenge

Starmer Faces Growing Dissent as Labour MPs Weigh Leadership Challenge

Reeves rejects £1bn plea for NHS redundancy payouts

Reeves rejects £1bn plea for NHS redundancy payouts

PM Condemns Leaks, Vows Loyalty to Ministers and Stability

PM Condemns Leaks, Vows Loyalty to Ministers and Stability

Major Rent Reform Ends No-Fault Evictions in England

Major Rent Reform Ends No-Fault Evictions in England

Senator John Fetterman Hospitalized After Fall from Heart Flare-Up, Keeps Sense of Humor

Senator John Fetterman Hospitalized After Fall from Heart Flare-Up, Keeps Sense of Humor

Greene Pushes Epstein Files Amid Trump Fallout

Greene Pushes Epstein Files Amid Trump Fallout

Trump Deploys DHS to Charlotte in Major Arrest Operation

Trump Deploys DHS to Charlotte in Major Arrest Operation

December Run-Off in Chile as Election Produces No Winner

December Run-Off in Chile as Election Produces No Winner

Canada Passes Carney’s First Budget in Tight Parliamentary Vote

Canada Passes Carney’s First Budget in Tight Parliamentary Vote

Shadow Fleet at Sea: Europe’s Battle Against Illicit Oil Shipping

Shadow Fleet at Sea: Europe’s Battle Against Illicit Oil Shipping

Most Tories Expect to Support a Farage-Led Government

Most Tories Expect to Support a Farage-Led Government

Georgians Defy Government Crackdown After Year of Protests

Georgians Defy Government Crackdown After Year of Protests

US National Guard Member Killed in DC Shooting

US National Guard Member Killed in DC Shooting

ICC to Rule on Duterte’s Provisional Release

ICC to Rule on Duterte’s Provisional Release

Starmer Says Labour’s Economic Plan Needs Years to Deliver

Starmer Says Labour’s Economic Plan Needs Years to Deliver

Khaleda Zia Death in Bangladesh: First Female PM Dies at 80

Khaleda Zia Death in Bangladesh: First Female PM Dies at 80

Russia losses Ukraine war peace talks intensify amid rising deaths

Russia losses Ukraine war peace talks intensify amid rising deaths

Albanese Opens Door to Bondi Royal Commission Amid Rising Pressure

Albanese Opens Door to Bondi Royal Commission Amid Rising Pressure

Trump Escalates Minnesota Immigration Surge Amid Rising Tensions

Trump Escalates Minnesota Immigration Surge Amid Rising Tensions

Iran Protesters Defy Crackdown as Violent Clashes Intensify

Iran Protesters Defy Crackdown as Violent Clashes Intensify

Homeland security agents deployed amid Minneapolis protests

Homeland security agents deployed amid Minneapolis protests

US Senate rejects resolution limiting Trump military powers

US Senate rejects resolution limiting Trump military powers

Right Must Unite After Jenrick Defection, Urges Rees-Mogg

Right Must Unite After Jenrick Defection, Urges Rees-Mogg

EU weighs response amid Greenland tariff crisis with Trump

EU weighs response amid Greenland tariff crisis with Trump

UK Ministers Drop Foreign Student Targets for Global Education Push

UK Ministers Drop Foreign Student Targets for Global Education Push

No Gas Boiler Ban as UK Warm Homes Plan Backs Heat Pumps

No Gas Boiler Ban as UK Warm Homes Plan Backs Heat Pumps

Shinzo Abe’s killer receives life sentence in Japan

Shinzo Abe’s killer receives life sentence in Japan

Sussan Ley leadership milestone shakes Liberal future

Sussan Ley leadership milestone shakes Liberal future

EU Says US Ties Have Suffered ‘Big Blow’ After Greenland Crisis

EU Says US Ties Have Suffered ‘Big Blow’ After Greenland Crisis

Satire Can Skewer Trump, But It Won’t Save Democracy

Satire Can Skewer Trump, But It Won’t Save Democracy

Police response times face strict new national limits

Police response times face strict new national limits

Labour policing overhaul sparks fears over growing central control

Labour policing overhaul sparks fears over growing central control

Starmer warns of toxic division politics in Reform challenge

Starmer warns of toxic division politics in Reform challenge

Keir Starmer Signals UK China Reset With Xi Visit Possibility

Keir Starmer Signals UK China Reset With Xi Visit Possibility

Cambridge Faces Scrutiny Over Arms Investment Transparency

Cambridge Faces Scrutiny Over Arms Investment Transparency

Israel Moves to Bar MSF From Gaza Operations

Israel Moves to Bar MSF From Gaza Operations

Palantir contracts face UK halt calls over transparency

Palantir contracts face UK halt calls over transparency

Australia’s Opposition Coalition Reunites After Rift

Australia’s Opposition Coalition Reunites After Rift

Nurses’ families fear breakup under UK immigration crackdown

Nurses’ families fear breakup under UK immigration crackdown

Cabinet Secretary Shake-Up Triggers Due Diligence Warning

Cabinet Secretary Shake-Up Triggers Due Diligence Warning

Australian Families Leave Syrian Camp for Home

Australian Families Leave Syrian Camp for Home

Trump Attacks UK-California Energy Pact

Trump Attacks UK-California Energy Pact

Farage to Name Jenrick as Reform Chancellor Pick

Farage to Name Jenrick as Reform Chancellor Pick

Civil Service Pay: Union Urges Ministers to End ‘Barking Mad’ Limits

Civil Service Pay: Union Urges Ministers to End ‘Barking Mad’ Limits

Antonia Romeo appointment sparks criticism

Antonia Romeo appointment sparks criticism

Trump and Chagos Deal Rift Over Iran Strikes

Trump and Chagos Deal Rift Over Iran Strikes

Andrew Arrest Sparks Republic Debate in Australia

Andrew Arrest Sparks Republic Debate in Australia

Global corruption crisis: Who Washington shields

Global corruption crisis: Who Washington shields

Farage Chagos Islands Row Sparks Fury

Farage Chagos Islands Row Sparks Fury

Reform UK targets workers’ rights repeal

Reform UK targets workers’ rights repeal

Russian Trade Routed Through British Islands Exposed

Russian Trade Routed Through British Islands Exposed

Boss Lincoln: The Partisan Politics of Abraham Lincoln

Boss Lincoln: The Partisan Politics of Abraham Lincoln

Mandelson Arrest: Met Apologises to Hoyle

Mandelson Arrest: Met Apologises to Hoyle

Palestine Action ban appeal moves forward

Palestine Action ban appeal moves forward

Germany Faces Backlash Over Scrapped Renewable Heating Mandate

Germany Faces Backlash Over Scrapped Renewable Heating Mandate

Trump Speech Sparks Intense Debate Across Divided America

Trump Speech Sparks Intense Debate Across Divided America

Has Europe truly learned from the failures of 2022?

Has Europe truly learned from the failures of 2022?

Liberal Review Shelved After Historic Election Loss

Liberal Review Shelved After Historic Election Loss

Trump Faces Questions Over Iran Conflict Plan

Trump Faces Questions Over Iran Conflict Plan

Herzog Asio meeting sparks security storm

Herzog Asio meeting sparks security storm

Texas Senate seat fight heads to runoff as votes split

Texas Senate seat fight heads to runoff as votes split

BBC Charter Reform Sparks Independence Battle

BBC Charter Reform Sparks Independence Battle

Thousands Protest Iran Strikes Outside US Embassy London

Thousands Protest Iran Strikes Outside US Embassy London

US Bombers Arrive at RAF Base Amid Rising Iran Tensions

US Bombers Arrive at RAF Base Amid Rising Iran Tensions

Pete Hegseth Iran War Remarks Spark Alarm

Pete Hegseth Iran War Remarks Spark Alarm

UK Oil and Gas Supplies Reassured Amid Middle East Concerns

UK Oil and Gas Supplies Reassured Amid Middle East Concerns

Trump Pressures Congress Over Save America Act

Trump Pressures Congress Over Save America Act

Iranian Football Squad Asylum Drama Shocks Australia

Iranian Football Squad Asylum Drama Shocks Australia

Queensland Protest Laws Spark Free Speech Backlash

Queensland Protest Laws Spark Free Speech Backlash

Eswatini Deal Sparks Global Outcry Over US Deportations

Eswatini Deal Sparks Global Outcry Over US Deportations

Yvette Cooper: UK Must Follow Principles, Not US Pressure

Yvette Cooper: UK Must Follow Principles, Not US Pressure

Trump Iran War Stance Hardens as Conflict Widens

Trump Iran War Stance Hardens as Conflict Widens

{kind=link}