The Office for National Statistics (ONS) has broken the fragile domestic calm of Westminster, releasing a “nasty” macroeconomic reality check that reveals the UK labor market is fracturing at an accelerating pace. According to official data published today, Tuesday, May 19, 2026, the headline unemployment rate unexpectedly ticked back up to 5.0% for the three months to March, climbing from the 4.9% recorded in the previous period. The increase completely blindsided City economists, who had confidently predicted the rate would hold steady, and marks the first definitive, “clinical” snapshot of how corporate Britain is buckling under the severe cost pressures unleashed by the escalating war in Iran. The sudden shift has brought a swift end to Chancellor Rachel Reeves’ hopes for an early-year economic victory lap, introducing an “asymmetric” layer of stress to the Treasury’s fiscal calculus.

Beneath the headline figure, more timely administrative tax data from HMRC paints an even more alarming picture of the structural “accountability rot” hollowing out employment security. Real-time PAYE records estimate that the UK economy shed a staggering 100,000 payrolled jobs in April alone, closely following a revised loss of 28,000 positions in March. This massive contraction represents the third-largest single-month collapse in payrolled employment since records began in 2014, excluding the anomalous depths of the pandemic lockdowns. Simultaneously, net job vacancies plummeted by another 28,000 to a five-year low of 705,000, signaling that businesses have aggressively slammed the brakes on recruitment to protect shrinking profit margins from global energy spikes and supply chain dislocations.

The data reveals that the retail, hospitality, and service sectors are bearing the brunt of this “resilience deficit,” as companies heavily reliant on part-time and short-term labor move at a “160 MPH clip” to shed headcount. Furthermore, a deeply troubling generational divide has emerged within the labor pool; the unemployment rate for young people aged 18 to 24 has ballooned to 14.7%, its highest level since late 2014. Independent analysts blame this spike on an accumulation of soaring minimum wage thresholds, shifting corporate structures, and the rapid deployment of artificial intelligence replacing entry-level administrative tasks, leaving a vast bottleneck of entry-level candidates entirely stranded.

For ordinary British households, the labor market softening arrives alongside a devastating slowdown in earnings potential. Regular pay growth, excluding bonuses, slowed to 3.4% year-on-year—the weakest pace of wage expansion since autumn 2020. When adjusted for the fresh wave of inflation fanned by Middle Eastern maritime blockades, real wage growth has dwindled to a microscopic 0.3%. While this cooling trend might offer some comfort to Bank of England policymakers who are desperate to prevent a wage-price spiral, it stokes very real fears of stagflation across the wider economy, leaving consumers trapped between a rising cost of living and a diminishing safety net of job availability.

The stark divergence between these labor statistics and the IMF’s recent upgrading of the UK’s 2026 GDP growth forecast to 1% highlights the highly volatile nature of the current economic environment. While the UK exhibited strong pre-war momentum during the first quarter of the year, corporate confidence has deteriorated rapidly over the last six weeks. With the Bank of England now forecasting that unemployment could steadily rise toward 5.5% by next summer, the government faces intense political pressure to move past reactive damage control and lay out a clear, proactive agenda for growth. For now, the “speechless determination” of thousands of newly out-of-work citizens navigating a shrinking job market serves as a stark reminder that international conflict can rapidly recalibrate the economic safety of the British high street.

Related News:

UK Must Act with Courage and Clarity on Israel-Palestine Conflict, Says Foreign Affairs Committee Report

UK Must Act with Courage and Clarity on Israel-Palestine Conflict, Says Foreign Affairs Committee Report

Radioactive Leak at UK’s Nuclear Warhead Base Sparks Outcry Over Safety and Secrecy

Radioactive Leak at UK’s Nuclear Warhead Base Sparks Outcry Over Safety and Secrecy

Mutual Inconvenience: Why Alaska Was Chosen for the Trump-Putin Summit on Ukraine

Mutual Inconvenience: Why Alaska Was Chosen for the Trump-Putin Summit on Ukraine

Terence Stamp, ’60s British Film Legend and Star of Superman, Dies at 87

Terence Stamp, ’60s British Film Legend and Star of Superman, Dies at 87

Where Is Prince William and Kate Middleton’s New House? Inside the Historic Lodge Set to Become Their ‘Forever Home’

Where Is Prince William and Kate Middleton’s New House? Inside the Historic Lodge Set to Become Their ‘Forever Home’

FIFA Eyes Biennial Club World Cup from 2029, Plans Possible Expansion

FIFA Eyes Biennial Club World Cup from 2029, Plans Possible Expansion

EuroMillions Record-Breaking £210m Jackpot Won by Lucky Lottery Ticket Holder

EuroMillions Record-Breaking £210m Jackpot Won by Lucky Lottery Ticket Holder

Is the UK Ready to Put Boots on the Ground in Ukraine? Assessing Military Capacity and Challenges

Is the UK Ready to Put Boots on the Ground in Ukraine? Assessing Military Capacity and Challenges

Shein UK Faces Allegations of Shifting Majority of Profits to Singapore to Reduce UK Tax

Shein UK Faces Allegations of Shifting Majority of Profits to Singapore to Reduce UK Tax

British Couple Among 16 Killed in Lisbon Funicular Tragedy

British Couple Among 16 Killed in Lisbon Funicular Tragedy

Protests Expected as Israeli Arms Firms Join Global Defence Trade Fair in London

Protests Expected as Israeli Arms Firms Join Global Defence Trade Fair in London

Thousands Gather in London to Protest Donald Trump’s Second UK State Visit

Thousands Gather in London to Protest Donald Trump’s Second UK State Visit

Trump Urges UK to “Call Out the Military” to Secure Borders Amid State Visit

Trump Urges UK to “Call Out the Military” to Secure Borders Amid State Visit

British AI Startup Outshines Human Forecasters in Global Prediction Contest

British AI Startup Outshines Human Forecasters in Global Prediction Contest

Liverpool Vs outhampton Set for Carabao Cup Clash at Anfield

Liverpool Vs outhampton Set for Carabao Cup Clash at Anfield

UK Fighter Jet Purchase Could Breach Nuclear Treaty, Warns CND

UK Fighter Jet Purchase Could Breach Nuclear Treaty, Warns CND

A Third of EU Citizens in UK Report Discrimination by Public Bodies Post-Brexit

A Third of EU Citizens in UK Report Discrimination by Public Bodies Post-Brexit

Public Trust in SNP Hits Historic Low Amid NHS Concerns

Public Trust in SNP Hits Historic Low Amid NHS Concerns

Cooper Unveils £4m Cyber Plan Against Russian Hackers

Cooper Unveils £4m Cyber Plan Against Russian Hackers

Johnson Suggests Mandelson Linked to China Spy Controversy

Johnson Suggests Mandelson Linked to China Spy Controversy

Rachel Reeves signals welfare reform ahead of key budget

Rachel Reeves signals welfare reform ahead of key budget

Kosovo agrees to host Britain’s refused asylum seekers

Kosovo agrees to host Britain’s refused asylum seekers

Johnson Approved China’s London ‘Super-Embassy’ in 2018

Johnson Approved China’s London ‘Super-Embassy’ in 2018

Top Christmas Books Reads: Classics to Cozy Romcoms

Top Christmas Books Reads: Classics to Cozy Romcoms

Just Stop Oil Protesters Convicted Amid Climate Defence Row

Just Stop Oil Protesters Convicted Amid Climate Defence Row

I’m a Celebrity 2025 line-up revealed: Osbourne joins

I’m a Celebrity 2025 line-up revealed: Osbourne joins

Palace May Restore Hyphen to Andrew Mountbatten-Windsor’s Name

Palace May Restore Hyphen to Andrew Mountbatten-Windsor’s Name

Royal Navy Shadows Russian Warships Entering the Channel

Royal Navy Shadows Russian Warships Entering the Channel

Starmer China visit raises human rights pressure on Beijing

Starmer China visit raises human rights pressure on Beijing

UK New Car Discounts Near £6,000 as Prices Are Slashed

UK New Car Discounts Near £6,000 as Prices Are Slashed

Snow and Rain Warnings as Cold Snap Continues in the UK

Snow and Rain Warnings as Cold Snap Continues in the UK

Dual Nationals Face Scramble for UK Passports as New Rules Come Into Force

Dual Nationals Face Scramble for UK Passports as New Rules Come Into Force

Trump and Chagos Deal Rift Over Iran Strikes

Trump and Chagos Deal Rift Over Iran Strikes

How Much Could Andrew’s Arrest Hurt the Royal Family?

How Much Could Andrew’s Arrest Hurt the Royal Family?

Australian PM Says Former Prince Andrew Has Suffered ‘Extraordinary Fall’ but That Won’t Prompt Republic Referendum

Australian PM Says Former Prince Andrew Has Suffered ‘Extraordinary Fall’ but That Won’t Prompt Republic Referendum

Farage Chagos Islands Row Sparks Fury

Farage Chagos Islands Row Sparks Fury

US Will Not Back Out of Tariff Deals with UK and Others, Says Trump Trade Representative

US Will Not Back Out of Tariff Deals with UK and Others, Says Trump Trade Representative

Storm Hernando: Edinburgh Airport Flights Cancelled in US Travel Chaos

Storm Hernando: Edinburgh Airport Flights Cancelled in US Travel Chaos

Trump Tariffs Threat Spark UK and EU Alarm

Trump Tariffs Threat Spark UK and EU Alarm

‘We’ve been paying for happy endings for Andrew for years’: inside the royal disgrace, biographer says

‘We’ve been paying for happy endings for Andrew for years’: inside the royal disgrace, biographer says

RAF Responding to Suspected Drone Strike at UK Cyprus Base

RAF Responding to Suspected Drone Strike at UK Cyprus Base

Islanders Advised on Travel to Middle East Amid Escalation

Islanders Advised on Travel to Middle East Amid Escalation

Brit ‘in Good Spirits’ Amid Dubai Missile Attacks, Stranded but Safe

Brit ‘in Good Spirits’ Amid Dubai Missile Attacks, Stranded but Safe

Trump rebukes Starmer over Iran strikes

Trump rebukes Starmer over Iran strikes

Stranger ‘On Drugs’ Stabbed Saudi Student to Death in Cambridge

Stranger ‘On Drugs’ Stabbed Saudi Student to Death in Cambridge

Minister Meets Crews Who Will ‘Take Out’ Iranian Drones

Minister Meets Crews Who Will ‘Take Out’ Iranian Drones

‘We Must Finish This’: Israelis Rally Behind War Effort as Iran Strikes Tel Aviv

‘We Must Finish This’: Israelis Rally Behind War Effort as Iran Strikes Tel Aviv

UK Prepares Aircraft Carrier for Middle East Crisis

UK Prepares Aircraft Carrier for Middle East Crisis

UK–US Tensions Ease as Starmer and Trump Hold First Call Since Iran Row

UK–US Tensions Ease as Starmer and Trump Hold First Call Since Iran Row

Yvette Cooper: UK Must Follow Principles, Not US Pressure

Yvette Cooper: UK Must Follow Principles, Not US Pressure

Iran War Warning: Starmer Backs Ukraine Visit

Iran War Warning: Starmer Backs Ukraine Visit

UK Wage Growth Slows as Jobs Market Holds Firm

UK Wage Growth Slows as Jobs Market Holds Firm

Australia Imposes Sudden Travel Ban on Iranian Visitors

Australia Imposes Sudden Travel Ban on Iranian Visitors

UK Forces Ready to Seize Russian Shadow Fleet Vessels

UK Forces Ready to Seize Russian Shadow Fleet Vessels

Net Closes on Lyons Clan: Partner Arrested in Dubai as Crime Boss Snared in Bali

Net Closes on Lyons Clan: Partner Arrested in Dubai as Crime Boss Snared in Bali

‘A Moral Stain’: LGBT Veteran Sues MoD for £50k Following Historic Abuse Claims

‘A Moral Stain’: LGBT Veteran Sues MoD for £50k Following Historic Abuse Claims

‘Better Off Not Planting’: UK Farmers Face 36% Fertiliser Spike as Gulf Crisis Bites

‘Better Off Not Planting’: UK Farmers Face 36% Fertiliser Spike as Gulf Crisis Bites

‘The Shield of Silence’: Grooming Inquiry to Expose Officers Who Sheltered Abusers

‘The Shield of Silence’: Grooming Inquiry to Expose Officers Who Sheltered Abusers

‘The Final Word’: Kathleen Stock’s Polemic Against Assisted Dying Reshapes the UK Debate

‘The Final Word’: Kathleen Stock’s Polemic Against Assisted Dying Reshapes the UK Debate

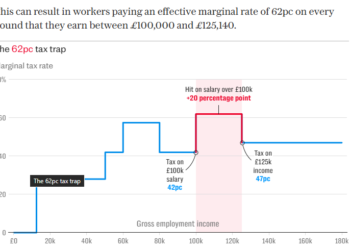

The ‘Career Ceiling’: One in Five High Earners Say £100k Tax Trap is ‘Ruining’ Their Ambition

The ‘Career Ceiling’: One in Five High Earners Say £100k Tax Trap is ‘Ruining’ Their Ambition

Open Justice Prevails as Court Rejects Bondi Gunman’s Family Anonymity Bid

Open Justice Prevails as Court Rejects Bondi Gunman’s Family Anonymity Bid

The Banbridge Rescue: 300 Sheep Saved from Massive Hay Shed Inferno

The Banbridge Rescue: 300 Sheep Saved from Massive Hay Shed Inferno

Debt Relief or Drop in the Ocean? UK Caps Student Loan Interest at 6%

Debt Relief or Drop in the Ocean? UK Caps Student Loan Interest at 6%

‘The £100,000 Hammer’: War in Iran Forces UK Businesses to Absorb Historic Fuel Hikes

‘The £100,000 Hammer’: War in Iran Forces UK Businesses to Absorb Historic Fuel Hikes

Border Breakthrough: UK and France Finalize New £662m Small Boats Deal

Border Breakthrough: UK and France Finalize New £662m Small Boats Deal

“Three-Wheeled Triumph”: Mayor of Erewash Completes 2,000-Mile European Charity Run

“Three-Wheeled Triumph”: Mayor of Erewash Completes 2,000-Mile European Charity Run

The “Charles Charm” Offensive: Did the Royals Find Their Mojo in D.C.?

The “Charles Charm” Offensive: Did the Royals Find Their Mojo in D.C.?

The $126 Spike: Oil Hits Four-Year High as Trump Weighs “Powerful” New Iran Strikes

The $126 Spike: Oil Hits Four-Year High as Trump Weighs “Powerful” New Iran Strikes

“An Endurance Test for the Mind”: British Couple Sentenced to 10 Years in Tehran

“An Endurance Test for the Mind”: British Couple Sentenced to 10 Years in Tehran

Premier League drama defines crucial weekend

Premier League drama defines crucial weekend

“Community Shield”: Met Police Deploy Specialist 100-Officer Team to Guard London’s Jewish Postcodes

“Community Shield”: Met Police Deploy Specialist 100-Officer Team to Guard London’s Jewish Postcodes

“The Cost of Conviction”: Palestine Action Activists Found Guilty Over ‘Clinical’ Factory Damage

“The Cost of Conviction”: Palestine Action Activists Found Guilty Over ‘Clinical’ Factory Damage

“The Rooftop Mystery”: Police Launch ‘Suspicious Death’ Probe After Body Found in Luxury Garden

“The Rooftop Mystery”: Police Launch ‘Suspicious Death’ Probe After Body Found in Luxury Garden

“The Local Gavel”: Polls Open Across Hampshire and Isle of Wight in Delayed ‘Milestone’ Vote

“The Local Gavel”: Polls Open Across Hampshire and Isle of Wight in Delayed ‘Milestone’ Vote

“The Blue Light Intersection”: Seventeen-Year-Old Critically Injured in ‘Nasty’ Police Pursuit Crash

“The Blue Light Intersection”: Seventeen-Year-Old Critically Injured in ‘Nasty’ Police Pursuit Crash

“The Fractured Frontier”: Sir John Curtice Declares the ‘Sacred’ Two-Party Era Over After ‘Milestone’ Results

“The Fractured Frontier”: Sir John Curtice Declares the ‘Sacred’ Two-Party Era Over After ‘Milestone’ Results

The Pathogen Protocol”: Third British National Monitored for ‘Nasty’ Suspected Hantavirus

The Pathogen Protocol”: Third British National Monitored for ‘Nasty’ Suspected Hantavirus

“The Reality Reckoning”: Government Demands Accountability as Channel 4 Pulls Married at First Sight UK Over Grave Sexual Assault Allegations

“The Reality Reckoning”: Government Demands Accountability as Channel 4 Pulls Married at First Sight UK Over Grave Sexual Assault Allegations

“I’ve Been Cheated”: Andrew Malkinson Lambasts the ‘Accountability Rot’ of the British Justice System Following True Perpetrator’s Conviction

“I’ve Been Cheated”: Andrew Malkinson Lambasts the ‘Accountability Rot’ of the British Justice System Following True Perpetrator’s Conviction

{kind=link}