As the global community enters the third month of the most “nasty and mischievous” geopolitical crisis of the decade, a “clinical” and “divergent” economic reality has emerged. While the 2026 Iran war has left millions of households in a “resilience deficit”—facing record-high energy bills and a “medication desert” of economic uncertainty—a select group of global giants are reporting a “160 MPH clip” of growth. From the “sacred” boardrooms of London and Houston to the high-tech defense hubs of Maryland, the “accountability rot” of conflict-driven profit has reached a “milestone” peak.

The conflict, which saw the Strait of Hormuz shuttered on March 4 and the subsequent “asymmetric” strikes on critical energy infrastructure, has “recalibrated” the flow of global capital. While the world prays for a “humanitarian” peace, the “160 MPH” engine of corporate earnings is proving that in the 2026 economy, crisis is the ultimate “golden tone” for the bottom line.

The “nasty” reality of $120+ oil has turned the world’s energy giants into the war’s most prominent “asymmetric” winners. Despite physical production hits—such as the strike on Shell’s Pearl GTL plant in Qatar—these firms have bypassed the “bottleneck” of supply through “clinical” trading strategies.

Shell’s $6.9 Billion Windfall: On Thursday, May 7, Shell reported adjusted first-quarter earnings of $6.92 billion (£5.1 billion), smashing analyst forecasts. CEO Wael Sawan described the result as a product of “relentless focus” during “unprecedented disruption.” The company’s “asymmetric” advantage lies in its trading desk, which saw earnings more than quadruple to $1.93 billion.

BP’s “Exceptional” Performance: UK rival BP reported a “milestone” doubling of its adjusted profits to $3.2 billion. Like Shell, BP’s traders were able to move at a “160 MPH clip,” capitalising on the extreme volatility that followed the “national security emergency” of the Hormuz closure.

The “Hole of a Billion Barrels”: Industry experts estimate that the war has created a “clinical” global supply gap of nearly one billion barrels. This “bottleneck” has “recalibrated” Brent crude to its highest levels in four years, allowing firms like Chevron and Equinor to see the value of their executive stakes rise by millions of pounds in a “medication desert” for consumers.

As the U.S. and its allies engage in “human-machine coordination” over Iranian skies, the “Prime” defense contractors have entered a “sacred” period of expansion. The war has “clinically” demonstrated that “justice has no expiry date” when it comes to replenishing military stockpiles.

Lockheed Martin’s 40% Surge: The world’s largest defense contractor has seen its stock price rise by nearly 40% since the start of 2026. As the U.S. spends an average of $1.8 billion a day on the conflict, Lockheed is bypassing the “bottleneck” of peacetime production to meet the “nasty” demand for precision-guided munitions and F-35 maintenance.

Northrop Grumman & RTX: These firms have seen a “golden tone” of returns, with the MSCI World Aerospace and Defence Index reporting net returns of 32% year-on-year at the end of March. The “asymmetric” nature of drone warfare in Iran has created a “milestone” demand for Northrop’s surveillance and strike capabilities.

The “Replenishment” Loop: With the Pentagon reportedly “burning” through its long-range missile reserves at a “160 MPH clip,” the “accountability rot” of the defense industry is under scrutiny. Critics argue that these firms “socialize risk downward” while concentrating the “upside” of conflict among a few “sacred” shareholders.

In the “clinical” surroundings of the New York and London stock exchanges, the Iran war has been “recalibrated” into a high-stakes trading game. Financial institutions are bypassing the “bottleneck” of traditional lending to find profit in the “nasty” swings of commodity prices.

The Banking Surge: JP Morgan Chase reported first-quarter earnings of $16.49 billion (up 13%), while Goldman Sachs and Morgan Stanley saw profits jump by 19% and 29% respectively. These banks cited “robust client engagement” and “high levels of trading” as the primary drivers, essentially monetizing the “resilience deficit” of the global market.

The “Prediction Market” Boom: In a “divergent” trend, platforms like Polymarket have seen record volumes as users bet on everything from the “milestone” date of a ceasefire to the “nasty” possibility of further infrastructure strikes. The top 1% of traders have reportedly captured 84% of all gains, creating a “postcode lottery” of war-based wealth.

The closure of the Strait of Hormuz on March 4 transformed the global shipping industry into a “floating bottleneck.” For those firms able to bypass the “national security emergency” through rerouting or insurance premiums, the war has been a “golden tone” for revenue.

The Tanker Premium: Shipping giants have seen tanker rates hit “milestone” highs as they circumnavigate the Middle East at a “160 MPH clip.” This rerouting adds thousands of miles to journeys, increasing fuel surcharges and “recalibrating” the cost of global goods.

The Insurance Spike: Marine insurers are reporting “asymmetric” gains as war-risk premiums for vessels in the Arabian Sea have skyrocketed. This “clinical” increase in costs is ultimately passed down to the consumer, worsening the “resilience deficit” in food and fuel prices.

In a “divergent” twist, the “nasty” reality of fossil fuel dependency has “boosted” the renewable energy sector. The Iran war marks the third “national security” energy shock this decade, creating a “milestone” urgency to bypass the “bottleneck” of oil.

TSMC & AI Resilience: Taiwan Semiconductor Manufacturing Company (TSMC) posted a net income of $18.1 billion (up 58%), driven by the “human-machine coordination” required for advanced defense and energy-efficient AI.

Renewable Policy Flurry: From South Korea to the UK, the “resilience deficit” of the 2026 grid has led to a “160 MPH” flurry of policymaking. The S&P Global Clean Energy Transition Index is up 70% year-on-year, as the world seeks a “sacred” and stable alternative to the “asymmetric” risks of Middle Eastern crude.

As the RHS Wisley wisteria reaches its peak and the Southbank Centre celebrates 75 years of progress, the “clinical” lesson of the Iran war is one of “asymmetric” outcomes. The “160 MPH” race for profit continues to bypass the “bottleneck” of human suffering, leaving an “accountability rot” that many believe can only be addressed through “milestone” windfall taxes.

“We have seen war and conflict manipulated so nakedly for short-term profiteering,” remarked one industry researcher. By acknowledging the “resilience deficit” of the global public, the call for a “golden tone” of corporate responsibility has never been louder. For now, the “clinical silence” of the boardrooms is broken only by the “160 MPH clip” of rising stock tickers, as the companies of the “Iron Triangle” continue to “recalibrate” the cost of havoc into the billions.

Related News:

Japan Braces as Takaichi Begins New Term with Huge Mandate for Low‑Tax, Ultra‑Conservative Agenda

Japan Braces as Takaichi Begins New Term with Huge Mandate for Low‑Tax, Ultra‑Conservative Agenda

G7 to Hold Emergency Oil Talks as Markets Plunge

G7 to Hold Emergency Oil Talks as Markets Plunge

Gulf Oil Shock Sends Global Economic Ripples

Gulf Oil Shock Sends Global Economic Ripples

Iran Rejects Ceasefire, Warns Trump With Chilling Message

Iran Rejects Ceasefire, Warns Trump With Chilling Message

The Situation Is Dire: War on Iran Squeezes India’s Cooking‑Gas Supplies

The Situation Is Dire: War on Iran Squeezes India’s Cooking‑Gas Supplies

Oil Price Jumps Despite Deal to Release Record Amount of Reserves

Oil Price Jumps Despite Deal to Release Record Amount of Reserves

‘Strategic Reserve’: Italy Defers Coal Phase-Out to 2038 Amid Energy Crisis

‘Strategic Reserve’: Italy Defers Coal Phase-Out to 2038 Amid Energy Crisis

The Iron Curtain Falls: Iran’s Steel Giants Forced Offline by US-Israeli Airstrikes

The Iron Curtain Falls: Iran’s Steel Giants Forced Offline by US-Israeli Airstrikes

Regional Escalation: Drone Strike Hits Kuwait’s Al-Zour Refinery Amid Trump’s “Stone Age” Ultimatum

Regional Escalation: Drone Strike Hits Kuwait’s Al-Zour Refinery Amid Trump’s “Stone Age” Ultimatum

Crude Surge: Oil Hits Four-Year High as Trump Weighs “New Options” for Iran

Crude Surge: Oil Hits Four-Year High as Trump Weighs “New Options” for Iran

“The Art of the Withdrawal”: Trump Targets Germany Troops as Iran Row Boils Over

“The Art of the Withdrawal”: Trump Targets Germany Troops as Iran Row Boils Over

“The Trading Bonanza”: Shell Profits Soar to $6.9 Billion Amid Iran War ‘Volatility’

“The Trading Bonanza”: Shell Profits Soar to $6.9 Billion Amid Iran War ‘Volatility’

“The Spoils of Conflict”: Global Giants Raking in Billions from the Iran War ‘Windfall’

“The Spoils of Conflict”: Global Giants Raking in Billions from the Iran War ‘Windfall’

Modi’s London Visit Seals Historic UK-India Trade Pact Amid Global Tensions

Modi’s London Visit Seals Historic UK-India Trade Pact Amid Global Tensions

China’s crackdown on civil servant perks sparks economic concerns

China’s crackdown on civil servant perks sparks economic concerns

Shein UK Faces Allegations of Shifting Majority of Profits to Singapore to Reduce UK Tax

Shein UK Faces Allegations of Shifting Majority of Profits to Singapore to Reduce UK Tax

Canada Passes Carney’s First Budget in Tight Parliamentary Vote

Canada Passes Carney’s First Budget in Tight Parliamentary Vote

UK New Car Discounts Near £6,000 as Prices Are Slashed

UK New Car Discounts Near £6,000 as Prices Are Slashed

Macron Rebuked in Franco-German Defence Row

Macron Rebuked in Franco-German Defence Row

Live Nation Sees Strong Ticket Sales as Monopoly Lawsuit Looms

Live Nation Sees Strong Ticket Sales as Monopoly Lawsuit Looms

Musk Cuts Starlink Access for Russian Forces – Giving Ukraine an Edge at the Front

Musk Cuts Starlink Access for Russian Forces – Giving Ukraine an Edge at the Front

US Will Not Back Out of Tariff Deals with UK and Others, Says Trump Trade Representative

US Will Not Back Out of Tariff Deals with UK and Others, Says Trump Trade Representative

Bill Gates ‘Took Responsibility’ Over Epstein Ties in Staff Meeting, Foundation Says

Bill Gates ‘Took Responsibility’ Over Epstein Ties in Staff Meeting, Foundation Says

RAF Responding to Suspected Drone Strike at UK Cyprus Base

RAF Responding to Suspected Drone Strike at UK Cyprus Base

Limited Flights Leave UAE But Disruption Continues Amid Iran Strikes

Limited Flights Leave UAE But Disruption Continues Amid Iran Strikes

The US Now Has the Medicine for Cheap Swarming Drone Attacks

The US Now Has the Medicine for Cheap Swarming Drone Attacks

Minister Meets Crews Who Will ‘Take Out’ Iranian Drones

Minister Meets Crews Who Will ‘Take Out’ Iranian Drones

UK Prepares Aircraft Carrier for Middle East Crisis

UK Prepares Aircraft Carrier for Middle East Crisis

Oil Prices Surge Above $100 Amid Iran War

Oil Prices Surge Above $100 Amid Iran War

UK–US Tensions Ease as Starmer and Trump Hold First Call Since Iran Row

UK–US Tensions Ease as Starmer and Trump Hold First Call Since Iran Row

UK Fuel Tax Hike Plan to Be Kept Under Review Over Iran Conflict

UK Fuel Tax Hike Plan to Be Kept Under Review Over Iran Conflict

‘Heating Oil Suppliers Are Holding Us to Ransom’ as Prices and Cancellations Surge

‘Heating Oil Suppliers Are Holding Us to Ransom’ as Prices and Cancellations Surge

UniCredit’s Bold Move to Reshape European Banking

UniCredit’s Bold Move to Reshape European Banking

Sri Lanka Sets Weekly Shutdown to Save Fuel

Sri Lanka Sets Weekly Shutdown to Save Fuel

UK Wage Growth Slows as Jobs Market Holds Firm

UK Wage Growth Slows as Jobs Market Holds Firm

Philippines energy emergency sparks coal power surge

Philippines energy emergency sparks coal power surge

Trump Threatens Iran With Total Infrastructure Destruction

Trump Threatens Iran With Total Infrastructure Destruction

‘Better Off Not Planting’: UK Farmers Face 36% Fertiliser Spike as Gulf Crisis Bites

‘Better Off Not Planting’: UK Farmers Face 36% Fertiliser Spike as Gulf Crisis Bites

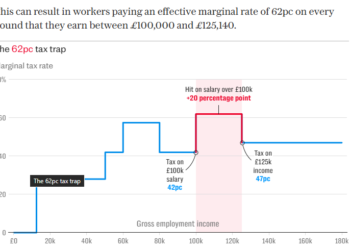

The ‘Career Ceiling’: One in Five High Earners Say £100k Tax Trap is ‘Ruining’ Their Ambition

The ‘Career Ceiling’: One in Five High Earners Say £100k Tax Trap is ‘Ruining’ Their Ambition

‘Blue Helmets’ in the Crossfire: Initial Probe Points to Roadside Bomb in Killing of UN Peacekeepers

‘Blue Helmets’ in the Crossfire: Initial Probe Points to Roadside Bomb in Killing of UN Peacekeepers

Russia: The Unforeseen Winner of the Iran Conflict

Russia: The Unforeseen Winner of the Iran Conflict

British Businesses Braced as National Living Wage Hits £12.71 Published: 1 April 2026

British Businesses Braced as National Living Wage Hits £12.71 Published: 1 April 2026

The Bitter Aftertaste: Iran War Threatens to Spike Prices for Indian Beer and Bottled Water

The Bitter Aftertaste: Iran War Threatens to Spike Prices for Indian Beer and Bottled Water

US Senators Slam Ticketmaster Over Sneaky New Fee Hikes

US Senators Slam Ticketmaster Over Sneaky New Fee Hikes

Hungary Claims Plot to Target Gas Pipeline Pre-Vote

Hungary Claims Plot to Target Gas Pipeline Pre-Vote

Oil and Diplomacy: Russian Refineries Burn as Zelenskyy Secures Middle East Shield

Oil and Diplomacy: Russian Refineries Burn as Zelenskyy Secures Middle East Shield

“A Perfect Storm”: UK Small Businesses Face Doubling Energy Bills as Iran War Rattles Markets

“A Perfect Storm”: UK Small Businesses Face Doubling Energy Bills as Iran War Rattles Markets

Electric Shock: Australians Buy Record Number of New EVs as Fuel Crisis Bites

Electric Shock: Australians Buy Record Number of New EVs as Fuel Crisis Bites

War, Windfalls, and the Carbon Trap: The Iran Conflict’s Brutal Energy Math

War, Windfalls, and the Carbon Trap: The Iran Conflict’s Brutal Energy Math

The Great Saddle-Up: Sydney Commuters Ditch the ‘Crazy’ Bowsers for the Bike Lane

The Great Saddle-Up: Sydney Commuters Ditch the ‘Crazy’ Bowsers for the Bike Lane

Debt Relief or Drop in the Ocean? UK Caps Student Loan Interest at 6%

Debt Relief or Drop in the Ocean? UK Caps Student Loan Interest at 6%

The Great Chokehold: Why the Strait of Hormuz is the Epicenter of the 2026 Crisis

The Great Chokehold: Why the Strait of Hormuz is the Epicenter of the 2026 Crisis

The Prediction Prohibition: White House Staff Barred from Betting on Political Markets

The Prediction Prohibition: White House Staff Barred from Betting on Political Markets

California fireworks blast: murder charges filed in case

California fireworks blast: murder charges filed in case

Relief at the Pump: Irish PM Unveils €505m Package to Stem Fuel Crisis

Relief at the Pump: Irish PM Unveils €505m Package to Stem Fuel Crisis

Diplomatic Deadlock: Lebanon Enters High-Stakes Border Talks with ‘No Cards to Play’

Diplomatic Deadlock: Lebanon Enters High-Stakes Border Talks with ‘No Cards to Play’

Blockbuster Resurrection: Avengers Reassemble and Top Gun Returns as Studios Tease 2026 Slate

Blockbuster Resurrection: Avengers Reassemble and Top Gun Returns as Studios Tease 2026 Slate

The Fog of War and the Ticker Tape: Suspicious Trades Rile Washington

The Fog of War and the Ticker Tape: Suspicious Trades Rile Washington

Brinkmanship in Islamabad: Tehran Vows ‘New Battlefield Cards’ as Ceasefire Wanes

Brinkmanship in Islamabad: Tehran Vows ‘New Battlefield Cards’ as Ceasefire Wanes

‘The End of the Quiet Era’: Japan Relaxes Arms Export Rules in Historic Pivot From Pacifism

‘The End of the Quiet Era’: Japan Relaxes Arms Export Rules in Historic Pivot From Pacifism

‘The £100,000 Hammer’: War in Iran Forces UK Businesses to Absorb Historic Fuel Hikes

‘The £100,000 Hammer’: War in Iran Forces UK Businesses to Absorb Historic Fuel Hikes

‘A Fragile Calm’: Oil Prices Dip as Trump Extends Iran Ceasefire, But Blockade Holds Firm

‘A Fragile Calm’: Oil Prices Dip as Trump Extends Iran Ceasefire, But Blockade Holds Firm

Red Lines in Ottawa: PM Carney Insists US “Won’t Dictate Terms” of Trade Review

Red Lines in Ottawa: PM Carney Insists US “Won’t Dictate Terms” of Trade Review

“Industrial-Scale Extraction”: White House Memo Accuses China of Mass AI Theft

“Industrial-Scale Extraction”: White House Memo Accuses China of Mass AI Theft

Beyond the Swoosh: Anta Sports Overtakes Rivals to Become Global Top Three

Beyond the Swoosh: Anta Sports Overtakes Rivals to Become Global Top Three

Return of the “Skiffs”: Threat Level Raised as Somali Pirates Seize Second Vessel in a Week

Return of the “Skiffs”: Threat Level Raised as Somali Pirates Seize Second Vessel in a Week

Southeast Asia Turns to Russia Amid Energy Crisis

Southeast Asia Turns to Russia Amid Energy Crisis

Ukraine Urges UK to Seize Russian Oil Tankers

Ukraine Urges UK to Seize Russian Oil Tankers

US Calls Australia Media Law “Foreign Extortion”

US Calls Australia Media Law “Foreign Extortion”

Capitalism ‘Suicidal’, Warns Petro at Climate Summit

Capitalism ‘Suicidal’, Warns Petro at Climate Summit

“Grounded”: Beijing Implements Total Ban on Drone Sales Citing Capital Security

“Grounded”: Beijing Implements Total Ban on Drone Sales Citing Capital Security

The Silent Scythe: How the Iran War is “Starving” Asian Paddy Fields Before the Harvest

The Silent Scythe: How the Iran War is “Starving” Asian Paddy Fields Before the Harvest

Ukraine strikes Tuapse as oil disaster worsens

Ukraine strikes Tuapse as oil disaster worsens

US to Escort Trapped Ships Through the Strait of Hormuz

US to Escort Trapped Ships Through the Strait of Hormuz

Trump Threatens UN Budget Cuts as US Pushes ‘Trade Over Aid’ Agenda

Trump Threatens UN Budget Cuts as US Pushes ‘Trade Over Aid’ Agenda

“The Pivot to Pakistan”: Trump Pauses ‘Project Freedom’ in Hormuz Amid Iran Deal Hopes

“The Pivot to Pakistan”: Trump Pauses ‘Project Freedom’ in Hormuz Amid Iran Deal Hopes

“The Strait Scramble”: Inside Trump’s ‘Project Freedom’ and the Hormuz Naval Escort

“The Strait Scramble”: Inside Trump’s ‘Project Freedom’ and the Hormuz Naval Escort

“The New Silk Road”: India and Vietnam Forge Strategic Maritime Alliance to Counter Regional Volatility

“The New Silk Road”: India and Vietnam Forge Strategic Maritime Alliance to Counter Regional Volatility

“The Peace Dividend”: Oil Prices Plunge and Global Stocks Surge on Reports of Iran Ceasefire Deal

“The Peace Dividend”: Oil Prices Plunge and Global Stocks Surge on Reports of Iran Ceasefire Deal

{kind=link}