Published: 20 May 2026. The English Chronicle Desk. The English Chronicle Online

The United Kingdom’s headline inflation rate has retreated to 2.8% for the 12 months leading to April 2026, marking a significant decline from the 3.3% recorded in March. This unexpected easing, which has brought the Consumer Prices Index (CPI) to its lowest level since early 2025, has provided a brief moment of “clinical” relief for both policymakers and households. However, beneath the headline figures, the economic landscape remains fraught with volatility. While the cooling of service sector costs and favorable base effects from last year’s price adjustments have driven this dip, leading economists are already signaling that this period of relative stability is likely a “fragile lull” rather than a lasting trend.

The primary drivers of this recent decline have been a combination of downward pressures in housing and household services, alongside a moderation in core services inflation. Yet, this “asymmetric” improvement is largely perceived as temporary. A “bottleneck” of broader price pressures remains hidden within the supply chain, particularly regarding energy. With significant household energy price increases scheduled for July, the expectation is that the headline rate will not remain at these levels for long. In fact, many financial institutions are now forecasting that inflation could surge toward 4% by the end of the year. This potential for an upward “leap” has muted any sense of victory, replacing it with a “speechless determination” among analysts to prepare for renewed volatility.

The Bank of England, having gained a small window of “breathing space” due to the lower-than-anticipated April data, now faces a difficult, “asymmetric” task. While the headline number is encouraging, the core drivers of long-term inflation—namely, how price hikes bleed into wage-setting and broader business costs—remain a concern. The labor market has shown signs of softening, which may mitigate some of the “nasty” inflationary feedback loops seen in previous years, but policymakers are wary of being too complacent. Given the history of global supply shocks that have plagued the economy for several years, there is little appetite for declaring a definitive end to the inflation fight. Most observers expect the central bank to maintain a hawkish stance, even if they choose to hold interest rates steady in the immediate future.

For the average household, this “asymmetric” tug-of-war between declining headline inflation and the looming prospect of higher energy and commodity costs creates a sense of profound uncertainty. While 2.8% is a welcome improvement, it masks the reality that the “resilience deficit”—the gap between stagnant real wages and the cumulative, high cost of living—remains vast. The risk is that the temporary relief experienced in April could lead to an “accountability rot,” where households and businesses are lulled into a sense of false security, only to be blindsided by a rapid return to 4% or higher by the end of the year. The “clinical” truth, as articulated by market researchers, is that the pipelines for price pressure are still full; the current dip is merely a temporary fluctuation, a momentary pause before the next wave of inflationary friction hits the consumer.

As the country moves into the summer months, the focus will shift from the relief of April’s data to the strategic preparation for the end-of-year outlook. The expectation of a return to higher inflation is already influencing market yields and government borrowing costs, which remain among the highest in the developed world. This “speechless determination” to weather the next inflationary cycle will likely define the economic policy debates in the coming months. Whether it is energy volatility driven by geopolitical tensions or structural challenges in the labor market, the drivers of the next upward trend are already apparent. For the policymaker, the challenge is no longer just about controlling the “asymmetric” spikes in inflation, but about managing a long-term, volatile landscape where stability is the exception, not the rule. The drop to 2.8% is a milestone worth acknowledging, but in the context of the current global economic reality, it is perhaps best viewed as a brief, tactical reprieve in a much longer, systemic struggle.

Related News:

UK Wage Growth Slows as Jobs Market Holds Firm

UK Wage Growth Slows as Jobs Market Holds Firm

Wealthy Britons Flee Gulf War but Avoid UK Taxes

Wealthy Britons Flee Gulf War but Avoid UK Taxes

BBC News Faces Deep Cuts in 2,000 Job Plan

BBC News Faces Deep Cuts in 2,000 Job Plan

New UK advice scheme to boost savings and investing

New UK advice scheme to boost savings and investing

“The Iron Chancellor of the North”: Andy Burnham’s High-Stakes U-Turn to Prevent a Truss-Style Gilt Market Meltdown

“The Iron Chancellor of the North”: Andy Burnham’s High-Stakes U-Turn to Prevent a Truss-Style Gilt Market Meltdown

Shein UK Faces Allegations of Shifting Majority of Profits to Singapore to Reduce UK Tax

Shein UK Faces Allegations of Shifting Majority of Profits to Singapore to Reduce UK Tax

British AI Startup Outshines Human Forecasters in Global Prediction Contest

British AI Startup Outshines Human Forecasters in Global Prediction Contest

China warns UK over delayed London mega embassy decision

China warns UK over delayed London mega embassy decision

Rachel Reeves to lead UK trade push in Saudi Arabia amid rights debate

Rachel Reeves to lead UK trade push in Saudi Arabia amid rights debate

UPS Cargo Plane Crash in Kentucky Kills Seven

UPS Cargo Plane Crash in Kentucky Kills Seven

UK New Car Discounts Near £6,000 as Prices Are Slashed

UK New Car Discounts Near £6,000 as Prices Are Slashed

Reform Plans to Keep UK’s Budget Watchdog in Office

Reform Plans to Keep UK’s Budget Watchdog in Office

Tories Call for Rethink of Parliament Revamp Plans

Tories Call for Rethink of Parliament Revamp Plans

UK Inflation Rate Falls to 3% in Year to January

UK Inflation Rate Falls to 3% in Year to January

Reeves Blocking Spending Boost for Defence

Reeves Blocking Spending Boost for Defence

Jenrick: I’ll Back OBR but There’ll Be No More Cosy Consensus

Jenrick: I’ll Back OBR but There’ll Be No More Cosy Consensus

Another U-turn Ahead as Labour Reconsiders Youth Minimum Wage

Another U-turn Ahead as Labour Reconsiders Youth Minimum Wage

US Trade Deficit Hits Fresh High Despite Trump’s Tariffs

US Trade Deficit Hits Fresh High Despite Trump’s Tariffs

UK Job Vacancies Fall to Lowest Level Since Pandemic

UK Job Vacancies Fall to Lowest Level Since Pandemic

US Will Not Back Out of Tariff Deals with UK and Others, Says Trump Trade Representative

US Will Not Back Out of Tariff Deals with UK and Others, Says Trump Trade Representative

Ukraine war briefing: Russia exporting more oil now than before war despite sanctions – report

Ukraine war briefing: Russia exporting more oil now than before war despite sanctions – report

Global markets face turmoil as Hormuz crisis deepens

Global markets face turmoil as Hormuz crisis deepens

Tim Wilson Sells Out Controversial Share Market Bet

Tim Wilson Sells Out Controversial Share Market Bet

Stock Markets and Oil Prices Still Volatile Over Fears Iran War May Drag On

Stock Markets and Oil Prices Still Volatile Over Fears Iran War May Drag On

Gulf shipping crisis sparks food price fears

Gulf shipping crisis sparks food price fears

Irish economy grew strongly in 2025

Irish economy grew strongly in 2025

Fuel Price Rise Makes Profit ‘Tricky’ for Taxis

Fuel Price Rise Makes Profit ‘Tricky’ for Taxis

UniCredit’s Bold Move to Reshape European Banking

UniCredit’s Bold Move to Reshape European Banking

UK Doubles Steel Tariffs to 50% to Protect Domestic Plants

UK Doubles Steel Tariffs to 50% to Protect Domestic Plants

Oil and Gas Prices Surge Amid Iran-Israel Attacks on Gasfields

Oil and Gas Prices Surge Amid Iran-Israel Attacks on Gasfields

Middle East Conflict to Hit UK Economy Hardest

Middle East Conflict to Hit UK Economy Hardest

UK Forces Ready to Seize Russian Shadow Fleet Vessels

UK Forces Ready to Seize Russian Shadow Fleet Vessels

FCA to Unveil Final Rules for Car Finance Redress Scheme

FCA to Unveil Final Rules for Car Finance Redress Scheme

Australia Halves Fuel Tax and Offers Free Transport Amid Crisis

Australia Halves Fuel Tax and Offers Free Transport Amid Crisis

‘Horror on the Street’ and ‘Fears Grow over Shortages’

‘Horror on the Street’ and ‘Fears Grow over Shortages’

‘Better Off Not Planting’: UK Farmers Face 36% Fertiliser Spike as Gulf Crisis Bites

‘Better Off Not Planting’: UK Farmers Face 36% Fertiliser Spike as Gulf Crisis Bites

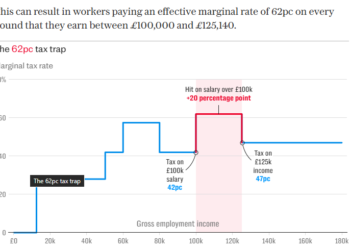

The ‘Career Ceiling’: One in Five High Earners Say £100k Tax Trap is ‘Ruining’ Their Ambition

The ‘Career Ceiling’: One in Five High Earners Say £100k Tax Trap is ‘Ruining’ Their Ambition

The Bitter Aftertaste: Iran War Threatens to Spike Prices for Indian Beer and Bottled Water

The Bitter Aftertaste: Iran War Threatens to Spike Prices for Indian Beer and Bottled Water

Debt Relief or Drop in the Ocean? UK Caps Student Loan Interest at 6%

Debt Relief or Drop in the Ocean? UK Caps Student Loan Interest at 6%

The ‘Shredder’ Syndrome: Why the 2026 Job Market is Breaking Entry-Level Spirits

The ‘Shredder’ Syndrome: Why the 2026 Job Market is Breaking Entry-Level Spirits

Diplomatic Sprint: Starmer Heads to the Gulf as 14-Day Truce Holds

Diplomatic Sprint: Starmer Heads to the Gulf as 14-Day Truce Holds

Global Commerce Crisis: Cooper Demands Immediate, Toll-Free Access to Hormuz

Global Commerce Crisis: Cooper Demands Immediate, Toll-Free Access to Hormuz

The Kitchen Table Crisis: How the 2026 Iran War Hits Your Wallet

The Kitchen Table Crisis: How the 2026 Iran War Hits Your Wallet

Student Loan Interest May Rise Despite 6% Cap

Student Loan Interest May Rise Despite 6% Cap

The Vance Verdict: How the Vice President Navigated the Islamabad “Pressure Cooker”

The Vance Verdict: How the Vice President Navigated the Islamabad “Pressure Cooker”

The Blockade Gambit: Trump’s High-Stakes Threat Leaves Middle East Predicaments Unchanged

The Blockade Gambit: Trump’s High-Stakes Threat Leaves Middle East Predicaments Unchanged

Carmakers Face £3bn Gap in UK Loan Payout Scandal

Carmakers Face £3bn Gap in UK Loan Payout Scandal

‘The £100,000 Hammer’: War in Iran Forces UK Businesses to Absorb Historic Fuel Hikes

‘The £100,000 Hammer’: War in Iran Forces UK Businesses to Absorb Historic Fuel Hikes

Fuel Crisis Drives UK Inflation to Highest Level Since December

Fuel Crisis Drives UK Inflation to Highest Level Since December

Navigating the Cost of Living: A Breakdown of the Latest Inflation Surge

Navigating the Cost of Living: A Breakdown of the Latest Inflation Surge

The “Long Tail” of War: Minister Warns Economic Scarring Could Last Eight Months Post-Conflict

The “Long Tail” of War: Minister Warns Economic Scarring Could Last Eight Months Post-Conflict

“A Zero-Value Home”: Seven Years of Sinkhole Stagnation Leaves Family Trapped

“A Zero-Value Home”: Seven Years of Sinkhole Stagnation Leaves Family Trapped

Albanese Rejects Gas Export Tax Push

Albanese Rejects Gas Export Tax Push

$13bn World Cup Set to Break All Revenue Records

$13bn World Cup Set to Break All Revenue Records

“A Food Security Timebomb”: Fertilizer Boss Warns Iran War Puts Billions of Meals at Risk

“A Food Security Timebomb”: Fertilizer Boss Warns Iran War Puts Billions of Meals at Risk

The $126 Spike: Oil Hits Four-Year High as Trump Weighs “Powerful” New Iran Strikes

The $126 Spike: Oil Hits Four-Year High as Trump Weighs “Powerful” New Iran Strikes

The “Taiwan Exception”: China Unveils Historic Zero-Tariff Access for 53 African Nations

The “Taiwan Exception”: China Unveils Historic Zero-Tariff Access for 53 African Nations

“A Summer of Consolidation”: Government Triggers Emergency Flight Rules as Jet Fuel Crisis Looms

“A Summer of Consolidation”: Government Triggers Emergency Flight Rules as Jet Fuel Crisis Looms

“Taking the Fight to Amazon”: GameStop Launches Unsolicited $55.5bn Bid for eBay

“Taking the Fight to Amazon”: GameStop Launches Unsolicited $55.5bn Bid for eBay

“The Breaking Point”: Hospitality Leaders Warn of a ‘Sinking’ Industry Amidst Rising Operational Costs

“The Breaking Point”: Hospitality Leaders Warn of a ‘Sinking’ Industry Amidst Rising Operational Costs

“The Power Paradox”: Can Scotland’s Politicians Truly Bypass the ‘Hormuz’ of Energy Pricing?

“The Power Paradox”: Can Scotland’s Politicians Truly Bypass the ‘Hormuz’ of Energy Pricing?

“The Price of Life”: Air Ambulances in the South Face ‘Resilience Deficit’ Amid Fuel Surge

“The Price of Life”: Air Ambulances in the South Face ‘Resilience Deficit’ Amid Fuel Surge

“The Energy Levy”: Understanding the ‘Milestone’ Windfall Tax on Oil and Gas Giants

“The Energy Levy”: Understanding the ‘Milestone’ Windfall Tax on Oil and Gas Giants

City & Guilds Faces Governance Crisis Over Sale

City & Guilds Faces Governance Crisis Over Sale

UK Must Act with Courage and Clarity on Israel-Palestine Conflict, Says Foreign Affairs Committee Report

UK Must Act with Courage and Clarity on Israel-Palestine Conflict, Says Foreign Affairs Committee Report

Trump’s UK Ambassador Urges North Sea Drilling to Strengthen US Ties

Trump’s UK Ambassador Urges North Sea Drilling to Strengthen US Ties

Millionaires group urge Reeves to introduce wealth tax to ‘lift kids out of poverty’

Millionaires group urge Reeves to introduce wealth tax to ‘lift kids out of poverty’

Starmer Says Labour’s Economic Plan Needs Years to Deliver

Starmer Says Labour’s Economic Plan Needs Years to Deliver

Historic £100-Weekly Pension Boost Brings Relief for UK Mineworkers

Historic £100-Weekly Pension Boost Brings Relief for UK Mineworkers

Major UK Clothing Firm Collapses into Administration — 109 Jobs at Risk

Major UK Clothing Firm Collapses into Administration — 109 Jobs at Risk

Iran War Puts Trump at Political Risk Amid Rising Prices

Iran War Puts Trump at Political Risk Amid Rising Prices

Charity Watchdog Takes Control of Learning Disability Care Home

Charity Watchdog Takes Control of Learning Disability Care Home

The 8 Million Dilemma: Why Britain’s Disability Safety Net is Facing a ‘2026 Reckoning’

The 8 Million Dilemma: Why Britain’s Disability Safety Net is Facing a ‘2026 Reckoning’

The Banbridge Rescue: 300 Sheep Saved from Massive Hay Shed Inferno

The Banbridge Rescue: 300 Sheep Saved from Massive Hay Shed Inferno

Oil and Diplomacy: Russian Refineries Burn as Zelenskyy Secures Middle East Shield

Oil and Diplomacy: Russian Refineries Burn as Zelenskyy Secures Middle East Shield

Electric Shock: Australians Buy Record Number of New EVs as Fuel Crisis Bites

Electric Shock: Australians Buy Record Number of New EVs as Fuel Crisis Bites

The Great Chokehold: Why the Strait of Hormuz is the Epicenter of the 2026 Crisis

The Great Chokehold: Why the Strait of Hormuz is the Epicenter of the 2026 Crisis

The Waiting Ward: ‘Month of Worry’ as Doctor Strikes Trigger Seismic Surgery Delays

The Waiting Ward: ‘Month of Worry’ as Doctor Strikes Trigger Seismic Surgery Delays

Roadside Reckoning: Nearly 160,000 Uninsured Vehicles Seized in National Crackdown

Roadside Reckoning: Nearly 160,000 Uninsured Vehicles Seized in National Crackdown

The Fog of War and the Ticker Tape: Suspicious Trades Rile Washington

The Fog of War and the Ticker Tape: Suspicious Trades Rile Washington

{kind=link}